- SWIFT: tradition and security in global money transfers

- SEPA: European ease for business

- TARGET: big money, fast and secure

- Instant payments: the fastest path to a more efficient business

- Correspondent banks: the foundation of the global financial network

- The impact of technology and future prospects

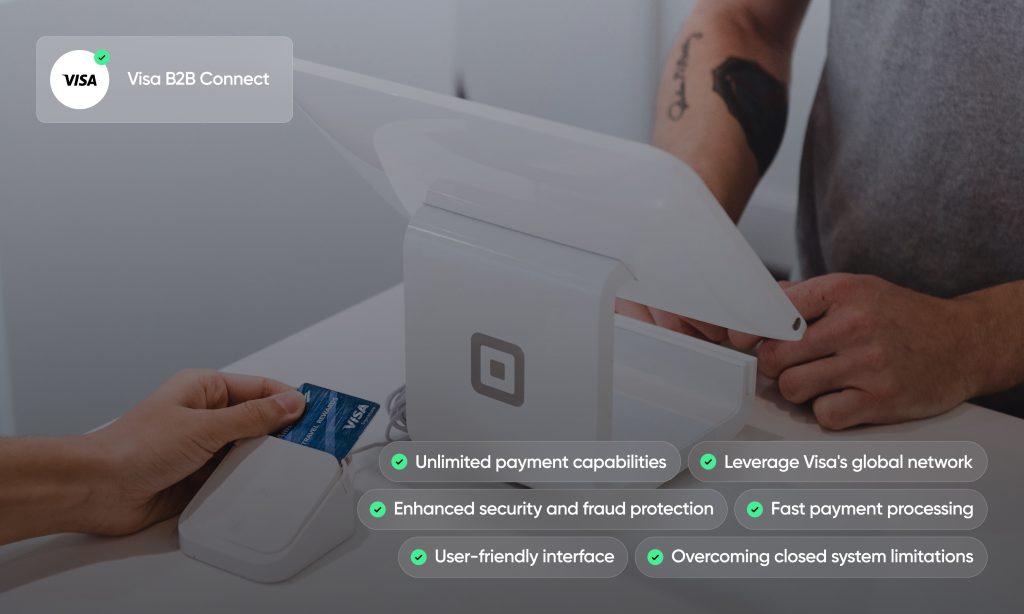

- Visa B2B Connect: global B2B payments through a single connection

- Future perspectives

The realm of payment systems is currently undergoing a revolution, providing businesses with new opportunities to enhance their financial operations, cut costs, and improve the security and efficiency of transactions. In this article, we’ll take a deep dive into three crucial aspects of today’s financial landscape: payment systems, correspondent banks, and the Visa B2B Connect platform. We’ll explore how these technologies and services are reshaping the business world and how financial institutions can take advantage of them.

SWIFT: tradition and security in global money transfers

For businesses involved in international money transfers, SWIFT (Society for Worldwide Interbank Financial Telecommunication) is a dependable tool. Linking over 11,000 financial institutions in more than 200 countries, SWIFT provides a global network for money transfers. It functions much like a global financial postal service, meticulously monitoring and securing each transaction. Despite being slower and more expensive than modern alternatives, the SWIFT system remains one of the most trusted methods for international payments. In 2023, an average of 44.8 million payments were processed daily, underscoring the essential role of the SWIFT platform in the global financial infrastructure and its reliability for financial institutions worldwide.

SEPA: European ease for business

For businesses and Fintech companies in Europe, SEPA (Single Euro Payments Area) is an essential tool for euro payments. SEPA unites 36 countries into a single payment area, enabling money transfers as easily as sending money to a local bank. This solution ensures efficient and secure transfers without intermediaries, significantly reducing transaction costs and time. SEPA offers various services that are particularly useful for businesses, such as one-time transfers (SEPA Credit Transfer or SCT), automated payments (SEPA Direct Debit or SDD), and instant payments (SCT Instant), which occur within seconds. SEPA payments have a limit of €100,000. According to the European Central Bank, the total number of cashless payments in the Eurozone exceeded 134 billion in 2023.

TARGET: big money, fast and secure

For Fintech companies and financial institutions handling large sums of money that require fast and secure payments, the European Central Bank offers the TARGET (Trans-European Automated Real-time Gross Settlement Express Transfer) system. The TARGET system acts like a high-speed train in the Eurozone financial market, providing real-time settlements with a high level of security. According to the European Central Bank, the number of payments processed through the TARGET system exceeded 479 million in 2023.

Instant payments: the fastest path to a more efficient business

Instant payments are a faster and more efficient solution for businesses looking to speed up financial operations. With instant payments, transactions can be completed in seconds, regardless of the time of day, ensuring immediate transfer of funds. In Latvia, instant payments are widely used and very popular, offering companies the opportunity to stay ahead of the competition with immediate payment processing. By integrating instant payments into their financial flow, businesses can be confident that they are prepared for future challenges and opportunities. According to a report by ACI Worldwide, the number of instant payment transactions in Europe grew from 13.2 billion in 2022 to approximately 17.2 billion in 2023. This figure is expected to continue rising, reaching 38.6 billion by 2028, with a compound annual growth rate (CAGR) of 21%.

In today’s global market, many other payment systems also offer solutions for efficient business operations:

- ACH (Automated Clearing House) – a popular U.S. domestic payment system that provides efficient and secure transfers.

- Faster Payments – quick and secure payments in the United Kingdom, enabling businesses to make swift transactions.

- RTGS (Real-Time Gross Settlement) – real-time, high-value transfers available in various countries, ensuring the immediate availability of funds.

- BACS (Bankers’ Automated Clearing Services) – a reliable system in the United Kingdom for direct debits and credits, providing secure and efficient payment processing.

- CHIPS (Clearing House Interbank Payments System) – a U.S. interbank payment system that handles high-volume transactions.

- Ripple – a blockchain technology offering fast and low-cost international transfers, presenting new financial opportunities in the global market.

- PayPal – a popular online payment platform that offers convenient and secure payments for online stores and other businesses.

- Alipay and WeChat Pay – extremely popular mobile platforms in China, offering extensive electronic payment options for businesses in this market.

- UPI (Unified Payments Interface) – India’s real-time payment system providing fast and efficient transfers.

- M-Pesa – a highly popular mobile payment system in Africa, offering accessible financial services to businesses in the region.

Understanding these payment systems helps businesses choose the most suitable solution to ensure fast, secure, and efficient financial transactions, adapting to the demands of different markets and fostering business growth.

Correspondent banks: the foundation of the global financial network

Correspondent banks are a crucial element in the electronic payment system. They act as intermediaries, facilitating fund transfers and currency exchanges between banks in different countries.

Correspondent banks offer several significant advantages that make them indispensable in conducting international financial transactions:

- Access to international markets: correspondent banks enable local banks and their clients to access global financial markets, facilitating international business and investment opportunities.

- Wide range of financial services: they provide a diverse array of financial services, including fund transfers, currency exchange, trade finance, and other essential services for conducting international transactions.

- Secure international transactions: by working with correspondent banks, local banks can ensure that their transactions are secure and comply with international financial standards.

- Correspondent banks often use the SWIFT network, which provides fast, convenient, and reliable electronic payments.

- Efficient processes: correspondent banks have developed and refined their processes to ensure that transactions are processed quickly and efficiently, minimizing delays and reducing operational risks.

These advantages make correspondent banks a vital component of the global financial infrastructure, supporting the smooth and secure flow of international transactions.

It’s important to be aware of and manage the risks associated with correspondent banking services. Firstly, these services can be costly, leading to significantly increased transaction costs, which can place a financial burden on Fintech companies and individual clients. Secondly, international money transactions require compliance with various complex and time-consuming regulations in each country, and failure to comply can lead to legal and financial consequences. Lastly, international payments can take longer to process compared to domestic transactions due to the additional intermediaries and processes required.

Banks address these challenges by investing in security technologies and collaborating with international organizations. They establish compliance programs to ensure adherence to regulations. Instant payments can help overcome the issues of traditional payment systems by providing immediate transactions and reducing the need for intermediaries.

The increased compliance requirements have led to a significant reduction in the availability of correspondent banking services in the market, making cross-border business transactions more challenging.

The impact of technology and future prospects

The advancement of modern technologies and financial innovations has resulted in significant improvements in electronic payment systems. Three key areas – blockchain, artificial intelligence (AI), and automation – are profoundly impacting this industry.

- Blockchain technology provides secure, transparent, and immutable transactions. Each transaction is recorded in a block, connected to the previous block, forming a chain. This ensures that transactions are unchangeable and transparent, reducing the need for intermediaries and lowering costs.

- Artificial Intelligence is used to enhance security, speed, and efficiency in payment systems. It can quickly analyze large volumes of data, identifying potential fraud cases and enabling faster transaction processing.

- Automation technologies help reduce manual labor, improve efficiency, and decrease the likelihood of errors. This allows banks and Fintech companies to process payments more quickly and accurately.

Payment systems not only need to be secure and efficient but also user-friendly. Improving the customer experience will be one of the key factors determining which technologies and solutions become popular in the future.

Visa B2B Connect: global B2B payments through a single connection

In the business world, speed and security are crucial, especially for international transactions. Fintech companies are increasingly turning to innovative solutions to optimize their payment processes, and one such solution is the Visa B2B Connect platform. It offers significant advantages in both speed and security by leveraging modern technologies.

Visa B2B Connect is an innovative solution that provides businesses with the ability to make international payments in local currencies across 120 countries, as well as in 21 other currencies worldwide. The platform uses blockchain technology, known for its security and transparency. Blockchain technology allows for tracking every transaction, ensuring that it is immutable and easily verifiable.

By utilizing Visa B2B Connect, businesses can streamline their cross-border payment processes, reducing the time and costs typically associated with international transactions. This platform’s integration of blockchain technology not only enhances security but also provides greater transparency, making it easier for companies to manage and monitor their global financial operations.

Key advantages of Visa B2B Connect:

- Unlimited Opportunities for outgoing payments to business partners in over 120 currencies, including GBP and USD.

- Leverage of Visa’s global network: built on Visa’s extensive global network, the platform offers versatile connectivity, allowing for clear timelines and transparent costs. This enhances predictability and economic efficiency in corporate transactions.

- Fast payment processing: the platform significantly reduces the time traditionally required for transactions, enabling quicker payment processing.

- Enhanced security and fraud protection: by utilizing a digital identity feature that tokenizes sensitive business information, such as bank details and account numbers, businesses are assigned a unique ID for transactions across the ecosystem. This reduces the risk of fraud.

- Overcoming closed system limitations: the platform is compatible with other existing payment systems and services, overcoming the limitations of closed systems.

- User-friendly interface: the platform is designed with a user-friendly interface, making Visa B2B Connect easy to use for everyday transactions.

These features make Visa B2B Connect a powerful tool for businesses seeking to optimize their international payment processes, offering a combination of speed, security, and ease of use.

In the realm of international B2B payments, businesses commonly encounter challenges such as varying regulations, fluctuating exchange rates, and long processing times. Visa B2B Connect aims to tackle these issues by providing a standardized platform that can be easily integrated into existing corporate systems through API or FTP integration, along with a network of partners.

Numerous global companies spanning various industries, including logistics, retail, and manufacturing, have already adopted this system. Users have provided overwhelmingly positive feedback, particularly praising the platform’s speed and security.

For businesses and financial institutions, exploring this solution has the potential to bring about substantial improvements in global payment operations. Magnetiq Bank, the first bank in Europe to offer this solution to its clients, grants access to Visa B2B Connect, making it a valuable option for companies seeking to enhance their international payment capabilities.

Future perspectives

Visa B2B Connect is set to expand into new markets and further improve its technology. The integration of artificial intelligence and additional automation will enhance the solution’s efficiency and security. Blockchain technology will also continue to shape future payment technologies, presenting new opportunities and business models. Visa B2B Connect is an innovation that is revolutionizing the business world by facilitating faster, more secure, and efficient payments.

Feel free to share this article to help others stay updated on the latest payment trends and challenges!